If Issuance is the answer, what is the question?

A look at recent staking rate conversations and effects.

As blockchains mature, a critical question that arises at the heart of these networks: tokenomics. In the roughly 16 years of their existence since Bitcoin's inception, we have seen a variety of experiments in this case along the lines of mining coins, premine sales, ICOs for percentages, liquidity pool mining, and recently airdrops becoming the primary means of distribution while teams building the protocols/investors get vested. Several protocols are reaching maturity, i.e.initial team and investor vesting schedules are concluding. These protocols can primarily be categorised into two main groups: network protocols, such as Ethereum and Solana, with their on-chain economies, protocols, and businesses, and DeFi/business protocols that serve users to achieve various on-chain objectives.

A crucial thing for network protocols on a long enough horizon is good tokenomics. They make or break the chain that they are the base asset for. High inflation erodes the value of the asset and makes it undesirable. For perspective, Solana’s inflation rate is 4.6% today, while Ethereum’s base issuance is ≈approximately 0.6 %. The asset is also used to secure the chain, so significantly underpaying or eliminating the rewards of chain validators is not a viable option. High gross inflation dilutes non-stakers, even if the net supply is flat after burns. A frequent or poorly communicated changes in the issuance of base assets could break the social contract of those who hold the assets as investments and wish to participate in the network's growth. The right issuance change could turn around the story of a network and give it the impetus to become successful as well. Ultimately, tokenomics dictates the longevity and utility of a chain’s base asset, preventing scenarios where network demand exists but the underlying token has faded into irrelevance.

In this blog, we explore some recent proposals of issuance change, we also look at some research that relates the staking rate to other things like the lending rate etc. We specifically look at SIMD228, Ethereum issuance conversations (including Minimum Viable Issuance concepts and specific EIP research) & the paper “Competitive equilibria between staking and on-chain lending” and other adjacent work, before finally talking about some crucial considerations in the world of base network assets. While SIMD-228 ultimately did not pass its governance vote, the underlying questions it raised persist and are likely to resurface.

Note: This post explores key debates and proposals primarily from the 2023-2024 period, a critical time for tokenomic evolution, updated with perspectives as of early 2025.

Solana: SIMD-0228 (failed Mar 2025)

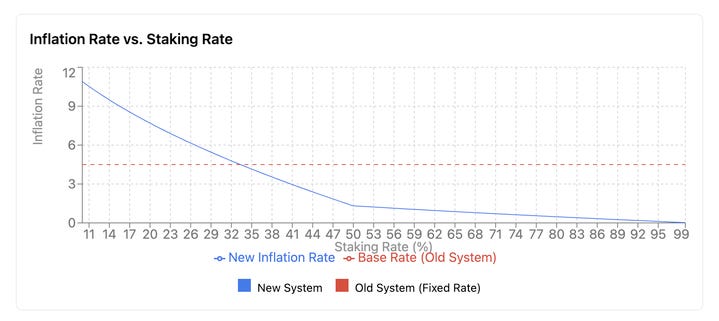

SIMD-0228 proposes transitioning Solana’s token issuance model from a fixed, time-based schedule to a more market-driven mechanism that adapts to real-time conditions—specifically, the fraction of total SOL supply that is staked. Under the current approach, token emissions were static, meaning they were fixed-schedule emissions that decreased predictably over time without regard to network dynamics. While we won’t initially discuss whether it should include network dynamics, the proposed formula ties issuance rates to the amount of the supply already securing the network. If a large portion is staked, the protocol can safely emit fewer new tokens, thereby reducing dilution. Conversely, if the staked fraction decreases, the system automatically increases emissions to incentivise more validators and protect network security. In other words, the staking issuance rate was going to be tied to the staked amount of tokens. Another motivation behind this change is that validators were already earning increasing revenue from MEV (maximal-extractable value), so they depend less on block rewards alone; hence, the network no longer needs as high an inflation rate for staking to remain attractive.

The current inflation schedule starts at 8% and decreases by 15% per year until it reaches 1.5% in ~2030. Under SIMD-0228, this issuance curve uses a function of the fraction staked plus a constant term, calibrated so that inflation remains low when staking is high and rises when staking dips below a threshold.

The proposed market-based emission mechanism employs a dynamic formula:

s is the staking rate

r is the static inflation rate (derived from a time-decay function starting at 4.68% and declining to 1.5%).

c is a constant that fine-tunes the inflation adjustment. The choice of this constant essentially determines the target staking rate.

i is the issuance/interest/inflation rate

This equation would dramatically reduce inflation when stake rates are high while providing automatic protection if network security becomes threatened. At current stake levels (~70%), this would decrease Solana's inflation rate from 4.68% to approximately 0.74%, resulting in a reduction of annual emissions by billions of dollars. The formula incorporates an elegant security threshold that becomes increasingly aggressive below 50% staked tokens, surpassing current emission rates if staking falls to 33%—a critical security threshold for consensus.

What does this ensure? By tying rewards to actual security needs and recognising that validators can earn outside income (e.g., MEV, tips), the proposal aimed to minimise unnecessary inflation (and its associated selling pressure) while preserving robust participation in validation. The ultimate goal is a more intelligent mechanism that evolves in response to network usage rather than a one-size-fits-all curve fixed in advance.

An extensive analysis of the effects of SIMD 228 is not the intent of this blog. You can take a look at it in SIMD-228: A critical analysis. Some broad observations reveal that SIMD-228 functions efficiently in high-stake scenarios, reducing unnecessary dilution while maintaining validator yields when combined with growing MEV revenue, which increased from $60– $ 70 M (full-year 2023) to $430M in 2024. However, simulating low-stake scenarios raises concerns about potential feedback loops, where reduced profitability could trigger validator exits, potentially destabilising the network. A 50-epoch (approximately 100-day) phase-in period was introduced later to mitigate immediate economic shocks, but it still represented a significant validator yield reduction of roughly 84% (4.68% → 0.74% = −84%) at current stake levels. SIMD 228 would have minimally impacted validator economics, as roughly half of the network, ~45–53% (30-day range) of validators, charge 0% commission on staking rewards and would, therefore, be unaffected by inflation changes.

Solana’s token issuance exists to achieve two core goals as is true about any layer 1 network: (1) incentivize validators to stake more SOL, thereby increasing security, and (2) encourage honest participation so that validators run their infrastructure reliably. The challenge is that higher emissions, in theory, secure these goals by “overpaying” for validator participation; however, they also come with a real cost—taxes, commission fees, or general market inefficiencies, as explained by Max Resnick in this blog. Over time, if Solana’s inflation rate remains disconnected from the actual state of security and validator performance, the network risks overspending on rewards while unnecessarily diluting the non-staking community. This is especially evident today, when block producers already earn a substantial income from MEV, and performance metrics, such as timely voting, show little room for further improvement. In other words, if security is largely sufficient and validator behaviour is already near optimal, continuing to issue large amounts of SOL is likely wasteful.

Beyond technical security, SIMD-228 also offered broader ecosystem benefits that align with Solana's vision as a high-performance financial system. As we will see, the staking rate is tied to the DeFi lending rate of a base asset. High inflation effectively penalises active SOL usage in DeFi, NFTs, and other on-chain activities, as non-staked tokens continue to suffer from continuous dilution. This creates an artificial pressure to hoard rather than utilize the network's native asset—precisely the opposite of what a vibrant blockchain ecosystem requires. The proposal's market-driven approach removes arbitrary human decisions from monetary policy, allowing natural market forces to determine optimal staking yields while releasing more SOL for productive applications.

We will now explore the rhetoric and research on issuance work in Ethereum land; some of the motivations to change remain the same.

Ethereum Issuance

Minimum Viable Issuance (Anders Elowsson) – Oct 2023

In "Minimum Viable Issuance" by Anders Elowsson, the concept of MVI is introduced and motivated. “Minimum viable issuance” (MVI) is the concept that Ethereum should not issue more ETH than is strictly necessary for security purposes. Issuance beyond the minimum required is viewed as an inflationary tax on regular users, compelling them to stake just to avoid dilution. Under Proof of Work, Ethereum followed MVI by reducing block rewards from 5 to 3 to 2 ETH to curb excessive miner profits. Under Proof-of-Stake (PoS), MVI refers to maintaining a stake (deposit) ratio that is high enough for security but not excessively high. Users shouldn’t feel compelled to stake out of fear of inflation or censorship; staking should reward security, not penalize non-stakers. Every ETH holder benefits if the issuance is minimized without hurting security. Anders argued that lowering issuance (thus staking yield) can increase overall utility for both stakers and non-stakers as long as security remains viable. High yields require stakers to lock up liquidity, expend resources, or trust third parties, which has an opportunity cost. Reducing issuance eases these burdens and reduces dilution of non-stakers, improving network value for everyone. MVI frames a pledge to users that Ethereum will only pay for “just enough” security. Over-issuance is perceived as undermining Ethereum’s utility and decentralisation in the long run.

Properties of Issuance Level (Anders Elowsson) – Jan 2024

In Properties of Issuance Level , some questions around issuance are considered such as “if issuance can be reduced while still retaining consensus stability, proper incentives, and acceptable conditions for solo staking”, “To what extent can Ethereum stop issuing more tokens than what is needed for security” etc.

By early 2024, ~25% of all ETH was staked (post-Merge and post-Shapella), and 28% as of April 2025. Anders argued that Ethereum may be overpaying for security at this level. Both The Merge (which added MEV/execution rewards to staking) and Shapella (which improved withdrawal liquidity) pushed up equilibrium staking participation. This raised the question: Can Ethereum lower issuance (reducing yields) and still maintain a stable and secure consensus?

Anders highlights that the protocol’s base reward factor F is the main “knob” controlling total issuance. Currently fixed (at 64), it yields an idealized protocol APR of

Under the current curve, as total stake D grows, yields drop off proportional to 1/sqrt{D} – but not fast enough to cap participation. In fact, nothing stops essentially all ETH from being staked profitably under status quo issuance.

The post analyzes how different issuance levels affect consensus incentives (e.g. honest behaviour, penalty risks) and reward variability. It asks if we could adopt a reward curve that either flattens or even turns downward beyond a certain stake level, D. For example, could we target an ideal total stake by adjusting yields once that level is reached? Alternatively, could we have negative net rewards beyond some point to disincentivise excess staking? These questions set the stage for exploring alternative issuance formulas that better adhere to MVI.

Anders concludes that Ethereum should indeed decrease issuance at high staking levels. He proposes changing the reward function to a “tempered” curve. This adjustment would cause rewards (and yield) to decline more aggressively as D grows, eventually halting further growth in stake. (In other words, beyond a point, adding more stake yields drastically lower returns, naturally finding an equilibrium stake level.) This concept was the basis for the later “Electra” proposal.

Endgame Staking Economics: A Case for Targeting (Ansgar Dietrichs & Caspar Schwarz-Schilling) – Feb 2024

In Endgame Staking Economics: A Case for Targeting & Electra: Issuance Curve Adjustment Proposal, an issuance curve change was suggested (Validator churn-limit cap EIP-7514 already slows further growth.). They observed February 2024, ~30M ETH (25% of supply) was staked, and climbing (Ansgar and Caspar argue that under current policy this trend will continue unabated – eventually, most or even all ETH could become staked. Critically, the rise of liquid staking tokens (LSTs) like stETH has reduced the friction and opportunity cost of staking, making high participation much more feasible.

The authors foresee a future where most ETH is staked via LSTs and outline why that is problematic. Some of these reasons were also elucidated in The Risks of LSD:

“Winner-takes-most” LST dominance: LSTs exhibit strong network effects (the more people hold a particular LST, the more useful and liquid it becomes). This could lead to a single, super-dominant staking provider or token. Such an LST might replace ETH as the de facto currency within Ethereum’s economy – exposing all users to that provider’s risks and governance by default. A dominant LST could become “too big to fail,” introducing a new centralized point of failure or control.

Centralization pressures: High staking ratios amplify economies of scale for staking service providers. Larger providers can operate more efficiently, attracting even more stake. This makes it harder for solo stakers to compete, eroding the decentralization of the validator set. In short, the higher the fraction of ETH staked, the more stake tends to concentrate in big pools.

Risk to ETH’s role and users: If an LST overshadows ETH as money, users holding plain ETH (for trustlessness) might still be indirectly “taxed” – e.g. missing out on staking yield while suffering dilution. Users may feel compelled to stake or hold LSTs (with added smart contract and trust risks) just to keep up, which undermines Ethereum’s credible, neutral, and self-custodial ethos. Additionally, more validators mean more network overhead (in terms of traffic and state) for nodes to handle.

Proposal – Stake Ratio Targeting: To avoid an over-staked future, they argue the “endgame” issuance policy should target an optimal staking range, e.g. around ~25% of ETH. Instead of letting all ETH eventually stake, Ethereum would actively adjust issuance to maintain a stable staking ratio. This ensures that security is sufficient but not excessive, thereby limiting the externalities as mentioned above. In their view, targeting a low-to-moderate staking percentage strikes the best balance between security and decentralisation.

Initial Analysis of Stake Distribution (Julian Ma) – Mar 2024

The work, "Initial Analysis of Stake Distribution," asked questions such as: Does the level of staking yield (issuance) affect how people stake (i.e., via solo node, decentralised pool, centralised exchange, or not at all)? There was a legitimate concern that lowering rewards might encourage more people to use liquid staking or centralised providers to maximise yield. Julian’s analysis models investor choices to investigate this concern.

The post outlines a simple utility model in which an investor allocates their ETH to the option that yields the highest combination of benefits, taking into account both yield and personal preference. Preferences represent non-monetary considerations, such as decentralisation, convenience, or trust. Hypothesis 1: An investor’s preference ranking for staking methods is independent of the yield level – meaning, lowering overall APR doesn’t suddenly make a decentralization-lover choose a centralized exchange, or vice versa. They will stake or not stake based on whether the yield meets their threshold, but their decision to stake is driven by other factors, such as technical expertise, values, etc.

The model finds that if an investor decides to stake at all, they will go all-in on the single option that maximises their utility, rather than splitting their stake. Crucially, it shows that the mix of staking modalities (solo vs. pooled) remains roughly the same regardless of issuance level. This result counters the fear that reducing issuance (and thus lowering yields) would deter people from solo staking and drive them toward LSTS or exchanges. It suggests that reducing rewards won’t necessarily decrease the share of solo stakers. Investors who highly value self-custody or trustlessness will continue solo staking even with lower returns, and those who prefer convenience will use services even at higher returns. Stake vs. not stake is influenced by yield, but how to stake is relatively insensitive to it.

The analysis assumes fixed preferences and zero friction. In reality, extreme changes or secondary effects could introduce nuances (e.g. if very low yields mean only large operators cover costs). But as a first-order approximation, it supports the argument that a moderate issuance reduction won’t centralize staking by itself. Other measures, such as education and tooling, are needed to boost solo staking, but we do not need to overpay on issuance to preserve the current distribution.

“Reward Curve with Tempered Issuance” (Anders’ EIP Research Post) – Apr 2024

In “Reward Curve with Tempered Issuance,” Anders Elowsson presents the case for adopting a “tempered” reward curve in Ethereum’s protocol, essentially laying the academic groundwork behind the Electra change. Anders notes that after The Merge and Shapella, staking participation grew significantly, and “there is broad consensus that the current deposit size keeps Ethereum sufficiently secure”. However, under the present curve, issuance will rise substantially as more stake comes in, eventually yielding diminishing returns (or worse) for Ethereum. If Ethereum continues to offer higher yields than needed, it “compels its users to incur higher costs, degrading user utility in aggregate.” In short, excessive incentives become perverse subsidies. This post systematically examines the benefits of moderating issuance and compares various methods for achieving this goal.

Proposed Curve (“Option A”): The candidate reward curve divides the current formula by (1 + D/k). Here, D is the total ETH staked, and k is a constant that sets the inflection point. Under this curve, issuance (and yield) still grows with more stake, but after a threshold, it grows much more slowly – eventually plateauing. Notably, the peak issuance rate occurs at D = k, beyond which additional staking actually reduces per-validator rewards, halving issuance at D = 2k, and so on. An initial k = 2^26, i.e., 67 million ETH, is suggested, which would place the peak around 55% of today’s supply, with a future adjustment to k = 2^25, i.e., 33.6 million (about 25% of the supply). These choices reflect a graduated approach: start by capping at a relatively high stake level, then potentially tighten the cap later once effects are observed.

Benefits & Trade-offs: The tempered curve is designed to maintain reliable consensus incentives and security while eliminating only the excess. The following criterias are examined:

Discouragement attacks & cartel risk: The network must avoid scenarios where low rewards could tempt validators to drop out or collude. The proposal maintains a non-zero baseline yield even at high D, ensuring there’s always incentive to stay online and honest. Critical attack thresholds (like a 1/3 cartel) would still require far more stake to go offline than plausible if k is well-chosen.

Stake Decentralisation: By limiting the total stake, the curve indirectly limits the growth of any single staking provider, as the entire pie stops expanding. This helps keep the staking set diverse, especially if k is adjusted downward over time.

Solo Staking Conditions: The post emphasises maintaining viable conditions for solo validators. With tempered issuance, equilibrium yields for stakers might actually be higher than under the status quo endgame. For example, if Ethereum ended up with 60M staked under the current policy, yields could drop to ~2%; however, if a tempered policy caps the stake at ~30M, yields might hover around 4% for those participants – benefiting individuals who stake, while still reducing total issuance. All ETH holders, stakers and non-stakers alike, gain from the reduced dilution and improved decentralization.

Comparison to Alternatives: Anders contrasts this approach with others, such as an even stricter capped issuance curve that sets a hard maximum or a dynamic targeting system. He finds the tempered curve strikes a good balance: it’s simple, autonomous, and doesn’t require complex governance or oracles, yet it achieves most of the gains by naturally finding an equilibrium stake level. In broad strokes, the author suggested tempered issuance policy could itself serve as the endgame solution, obviating the need for active stake targeting. While other’s noted it as a great short-term policy but still favor an eventual explicit targeting mechanism.

“Issuance Issues” Series (Mike Neuder) – Mar–Jun 2024

Ethereum researcher Mike Neuder wrote a three-part series, Issuance Issues, distilling the debate in an accessible way. These pieces provide intuition and address misconceptions around Ethereum’s issuance strategy:

Initial Issue (Part 1, Mar 2024)

Mike opens by noting that the reality of staking in 2024 has changed since the Beacon Chain launched – thanks to developments such as liquid staking, MEV, and Shapella. The future is uncertain, but the decisions made now will shape Ethereum’s security and decentralisation for years to come. With the Electra fork, he urges making a conscious, intentional decision on issuance . Even doing nothing is an active choice; given Ethereum’s march toward an ossified protocol.

The article walks through why more is not always better for stake. It echoes the negative externalities, including the dilution of ETH holders beyond the necessary security, LST dominance, and solo staker struggles, among others. Beyond a certain point, the marginal utility of more stake becomes negative. The piece also addresses why EIP-1559’s burn mechanism doesn’t cancel out issuance concerns (this is fully explored in Part 3). In short, net supply might be constant or deflationary, yet issuance is still redistributing ownership from non-stakers to stakers. Even if ETH’s total supply isn’t increasing, over-issuance can still harm decentralisation and fairness.

Mike outlines possible paths: keep status quo, adopt a one-time curve adjustment (like Anders’ proposal), or aim for a dynamic targeting policy. He compares staking equilibria under different issuance rates (“apples-to-apples”), illustrating how a lower issuance rate could result in fewer total validators but each getting a higher fraction of rewards – thereby achieving a similar or even higher real yield for stakers in equilibrium. A special focus is on the solo staker’s perspective: what level of rewards is needed to justify solo staking given costs and risks? And how do large staking pools change that calculus? The takeaway is that a moderate issuance reduction can still keep solo staking economically rational, especially if it prevents an overly large validator set where only big providers thrive.

Subsequent Soliloquy (Part 2, May 2024)

The second article responds to feedback from the initial post. One critique was that the case for changing issuance relied on speculation about the future. Mike acknowledges the uncertainty (e.g., we cannot know exactly how ETFs, restaking, or macro factors will influence staking). However, he argues that Ethereum’s success will hinge on decisions made under uncertainty, and that this policy should be proactive not reactive.

A key focus here is the distinction between the nominal issuance rate and the real yield for stakers. The author walks through “supply curve” scenarios to show that paradoxically, lowering issuance now could result in higher staking yields in the long run. How? If issuance is lower, fewer people will stake (all else equal), which means the reward pie is shared among fewer validators. Those validators could earn a similar or greater percentage yield than in a world where everyone is staking for a larger pie: in equilibrium, the marginal staker’s “reservation yield” is met. A reduced issuance policy means that equilibrium occurs at a smaller D with a slightly higher yield, rather than a huge D with a very low yield. Thus, stakers aren’t necessarily hurt by a policy change – they might give up some nominal rewards now in exchange for healthier long-term conditions (less competition, more decentralisation, and likely higher percentage returns once the system equilibrates).

Tertiary Treatise (Part 3, Jun 2024)

The third installment tackles a common confusion in “The Great Issuance Debate”: “How can issuance be too high if ETH’s net supply is barely inflationary or even deflationary (thanks to EIP-1559 burns)?. Some community members pointed to Ethereum’s shrinking supply in 2023–24 as evidence that issuance is fine. Mike’s rebuttal: burning fees is largely orthogonal to the issuance policy. Whether the total ETH supply goes up or down isn’t the central issue – what matters is the redistribution effect of issuance.

Ownership Redistribution: The author systematically shows that issuance always shifts relative ownership from non-stakers to stakers, regardless of burns. Imagine two groups: stakers and HODLers. When new ETH is issued to stakers, their share of the total pie increases at the expense of HODLers. Now, burning fees (which come roughly pro-rata from all users via gas) reduces the pie for everyone, but doesn’t change the fact that stakers received newly minted ETH. In fact, a higher burn rate can increase the gap in relative holdings: if the net supply is deflationary, a non-staker’s balance might drop in percentage terms while stakers both avoid that drop and gain new ETH. Thus, a big burn makes it even more important to stake if one wants to maintain their share of the network.

The treatise concludes that net inflation ≠ economic dilution. Even with 0% net supply growth, issuance can be too high if it forces people into staking to avoid losing ground. The burn is a mechanism for value accrual and fee market efficiency, but it does not justify an otherwise suboptimal issuance level. Ethereum should decide issuance based on security and incentive alignment, treating burns as a separate consideration. Once this is understood, it becomes clear that we should evaluate issuance in its own right – and if it’s causing undesirable effects (such as excessive stake centralisation), it should be adjusted irrespective of the burn.

The external effects of staking rate with DeFi

In the work, Competitive equilibria between staking and on-chain lending, Tarun Chitra explores lending markets in Proof of Stake (PoS) systems and starts with a fundamental reality: crypto tokens in these networks play two roles at once. They serve as both the security deposit that protects the network (when staked) and the money that people trade (when circulating). This creates a basic tension - the same token can't be in both places at once. This dual-purpose nature doesn't exist in Bitcoin's Proof of Work, where security comes from external resources (electricity and mining hardware) rather than the token itself. Ethereum currently has a significant portion (estimated around 20-25% as of early 2025) of all staked ETH simultaneously restaked in EigenLayer, illustrating this latent leverage.

The model assumes that people who stake tokens (validators) will behave rationally and allocate their funds to where they earn the best return. If lending suddenly offers better rewards than staking, validators may withdraw their tokens from staking to lend them instead. If many do this at once, it could seriously weaken network security. This mirrors what happens in traditional finance with mortgage-backed securities (MBS), where homeowners' long-term debts are transformed into liquid investments, creating risk if everyone tries to cash out simultaneously. This analogy was explored in a subsequent blog by him, titled “What PoS and DeFi can learn from mortgage-backed securities.”

To understand how validators make decisions, Markowitz portfolio theory is employed - in simple terms, this just means people try to balance risk and reward when investing. Think of it this way: if you have $1,000, you don't usually put it all in one extremely risky investment or all in a very safe one. Most people spread it around based on their level of comfort with risk. In the paper’s model, validators constantly weigh the rewards of staking (network inflation rewards) against lending (interest rates), considering the risks of each. Some validators are more risk-averse than others, which prevents everyone from making the same move at once.

The paper looks at two main scenarios: a simpler one where tokens are either staked or lent, and a more complex one that includes borrowing. In the simpler model, the lending interest rate depends on the percentage of available tokens that are already being borrowed, much like banks charge higher interest when loan demand is high. This mimics how mortgage rates work in traditional finance, though crypto lending has the huge advantage of complete transparency and automated execution through smart contracts.

One of the model's key discoveries is that there's a tipping point where the system can flip from mostly-staked to mostly-lent. Think of it like a crowded theater where a few people leaving is fine, but once enough people head for the exit, everyone rushes out at once. This same behavior happened in mortgage markets during the 2008 crisis, when seemingly stable investments suddenly collapsed as investors all tried to sell at the same time.

The math indicates that deflationary cryptocurrencies (those with a decreasing supply over time, such as Bitcoin) are particularly vulnerable to this security drain. Without sufficient rewards to keep validators staking, lending becomes the more attractive option. Meanwhile, inflationary systems (where supply increases over time) tend to maintain better security because they can keep staking rewards competitive with lending rates. This pattern mirrors the boom-bust cycles in mortgage markets, where periods of easy credit followed by tightening create instability.

The model helps protocol designers find the "sweet spot" where validators can borrow against their stake without undermining network security. This requires careful balancing of borrowing limits, interest rates, and liquidation thresholds, similar to how traditional securitisation markets structure mortgage-backed securities. The big advantage in crypto is that these rules can be enforced by code rather than depending on human judgment and institutional oversight that failed so spectacularly in the mortgage crisis.

Thinking loudly about Issuance

Philosophy of “Moneyness”

The fundamental question at the core of blockchain economic design is not simply technical but philosophical: what truly constitutes "moneyness" in digital assets? Unlike fiat currencies, which derive their legitimacy from government backing, legal tender status, and centuries of institutional usage, blockchain assets must establish their monetary properties through protocol design alone. The introduction of dynamic staking yields—as proposed in SIMD-228, and the eventual target of ethereum issuance (a dynamic staking curve)—creates a tension between market responsiveness and predictability. While floating rates may optimize capital efficiency, they fundamentally alter the asset's perceived stability characteristics. This added complexity in monetary policy potentially undermines the simplistic narrative that users need to understand an asset as "money," which traditionally benefits from straightforward, predictable properties rather than algorithmic complexity. Although traditional money is indeed a system managed through a dynamic monetary policy, it is imperfect.

Engineering for Antifragility

Consider that lowering issuance doesn’t equate to weakening security – if done correctly, it trims excess “buffer” stake while keeping enough validators online. Excessive stake beyond the necessary threshold doesn’t materially increase security, but it does increase the risk of centralisation. But we must ask how low is too low for issuance, highlighting the importance of not undershooting and causing a security shortfall.

While targeting stake is a good idea, The emergence of sophisticated financial engineering in blockchain—particularly liquid staking derivatives (LSDs) and cross-protocol restaking—introduces systemic risks that protocol monetary policies often fail to fully account for. When stake can be simultaneously counted across multiple applications and synthetically looped through derivatives, the actual risk exposure becomes exponentially more complex than a simple measure of "percentage staked" might suggest. These instruments create hidden leverage, potentially triggering devastating cascade failures during market stress. The interconnectedness of these systems means that a protocol's monetary policy cannot be designed in isolation; it must consider how capital flows through an increasingly integrated financial ecosystem where the same collateral is effectively counted multiple times. Consider the following: if, in a system targeting a 25% stake, 10% is restaked, can we consider this 10% portion with the same “purity” and risk parameters as we do for the un-restaked assets? In the event of a slashing of these restaked assets, isn’t the network suddenly at risk? Restaking has made systems more fragile to edge cases and cascades that are difficult to design against.

There is also a rational argument that stake targeting might actually not result into the intended effect. In a world where asset values remain static/appreciate, holders might buy tokens, stake for a minimal yield and seek more restaking opportunities for additional “safe” yield, thus increasing the quantity of restaked yield in the entire system.

There is an argument that complex systems require continuous feedback mechanisms to achieve antifragility—a principle observed across evolution, market economics, and scientific progress. Fixed inflation schedules represent a form of central planning that lacks the responsive adaptation characteristic of resilient systems. The rigid, time-based inflation curve currently used by Solana (and initially borrowed from Cosmos) exemplifies this rigidity—an arbitrary human decision rather than a market-determined equilibrium. Market-based approaches potentially introduce greater adaptability, allowing the system to self-adjust to changing conditions and unexpected shocks. However, we must question whether the specific feedback loop in SIMD-228 (staking percentage) provides sufficient information about the system's true security and health, especially given the complexities introduced by derivative instruments.

The interaction between staking yields and lending rates represents another critical dimension often underexplored in monetary policy discussions. When on-chain lending markets offer yields competitive with or superior to staking returns, capital naturally flows toward higher returns, potentially undermining network security. This phenomenon, where DeFi protocols effectively "cannibalise" security by outbidding the consensus mechanism for capital, creates complex game theory scenarios that static models struggle to capture. A dynamic monetary policy may prevent this competition in high-stake scenarios by reducing inflation (and thus staking returns), but could potentially create dangerous oscillatory effects if lending rates and staking yields repeatedly prompt large capital shifts between the two. Second-order effects and feedback loops present perhaps the greatest challenge in designing resilient token economics. Network stability depends not just on direct parameter adjustments but also on how participants behave in response to these changes.

Ultimately, blockchain monetary policy represents an unprecedented experiment in designing crypto-economic systems without centralized control. While traditional finance relies on central banks, lenders of last resort, and regulatory frameworks to manage crises, decentralised systems must attempt to encode all edge cases and design for adversarial scenarios in their protocol design. They must anticipate worst-case scenarios and ensure their systems can withstand these, eliminating the need for hard forks or network restarts; liveness is a crucial and desirable property in blockchain systems. This requires a balanced approach that incorporates market feedback while maintaining sufficient stability and predictability for everyday users. The tension between creating capital efficiency through dynamic mechanisms versus establishing trusted monetary properties through predictable issuance remains fundamentally unresolved. As these systems mature, they may need to develop more sophisticated response mechanisms that account for derivative instruments, cross-protocol interdependencies, and behavioural economics rather than relying solely on simple metrics like staking percentages to guide monetary policy. Future work must measure effective stake, discounting assets rehypothecated in restaking or DeFi, to maintain honest security budgets until we do, ‘issuance tweaks’ risk becoming whack-a-mole against invisible leverage rather than an actual monetary policy.